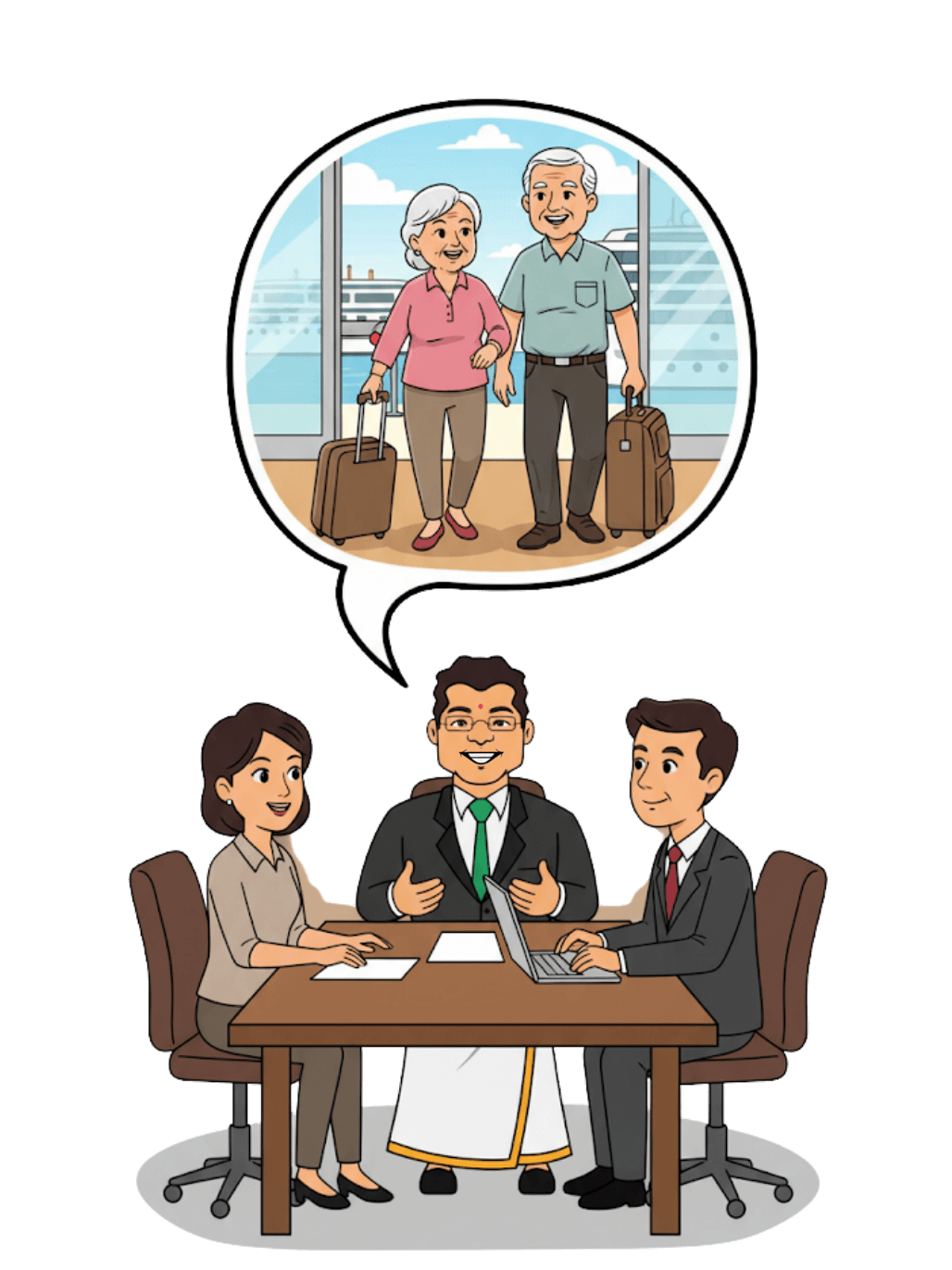

Tailored Retirement Solutions

Your life goals drive your plan. We listen, understand, and craft strategies as unique as you.

Stress-Free Process

We break things down, making it easy to take action, step by step.

Growth-Focused Investments

We identify the right mix of funds and instruments to help your wealth grow and last.

Clarity at Every Turn

From pension rules to tax angles and withdrawal options, we ensure you’re always informed.

Reviews & Realignment

Life changes. So do plans. We check in often, making sure your path stays on track.

A Sense of Security

We are here for every question, transition, or dream—offering peace of mind for you and your family.

Justo laoreet sit amet cursus sit amet dictum sit. Eu scelerisque felis imperdiet proin